Les nouveaux usages d'aujourd'hui seront les business de demain.

Revue de presse sur les tendances et évolutions technologiques utiles.

http://theitwatcher.fr/.

A lire sur: http://spectrum.ieee.org/semiconductors/devices/the-status-of-moores-law-its-complicated/

Node names—the milestones of the chip industry—no longer mean what they used to

By Rachel Courtland

Posted

Illustration: Harry Campbell

One chilly Tuesday evening last December, dozens of

physicists and engineers who dream up tomorrow’s transistors met in San

Francisco to ponder the far future. Would today’s state-of-the-art

switch—a three-dimensional transistor dubbed the FinFET—be able to carry

chips “to the finish,” a distant, possibly unreachable horizon where

transistors are made up of just a handful of atoms? Or would we need a

new technology to get us there?

This may all sound like the tech world’s version of arguing over how

many angels can dance on the head of a pin, but it actually has enormous

real-world implications. The semiconductor industry pulled in revenues of US $300 billion

in 2012. After decades of fulfilling Gordon Moore’s prophesy of

steadily doubling transistor densities (these days every 18 to 24

months), the industry is now delivering integrated circuits with

transistors that are made using what chipmakers call a 20- or

22-nanometer manufacturing process. An IC fabricated with this process,

such as a microprocessor or a dynamic RAM (DRAM) chip, can have billions

of transistors.

Nevertheless, there on the cutting edge, the business is troubled. Each

new generation of ultradense chips demands a new manufacturing process

of mind-boggling industrial and technological complexity. The struggle

has become so pitched that researchers are now often at a loss for words

to describe the metrics of their progress.

At the December meeting, for example, Chenming Hu, the coinventor of the FinFET,

began by mapping out the near future. Soon, he said, we’ll start to see

14-nm and 16-nm chips emerge (the first, which are expected to come

from Intel, are slated to go into production early next year).

Then he added a caveat whose casual tone belied its startling

implications: “Nobody knows anymore what 16 nm means or what 14 nm

means.”

It’s actually become a fairly common refrain among industry experts.

The practice of attaching measurements to chip generations has “been

hijacked by marketers to an enormous extent,” one chip-design expert

told me. “A lot of it’s really smoke and mirrors,” says analyst Dan Hutcheson

of VLSI Research in Santa Clara, Calif. It’s “spin,” he says, that’s

designed to hide widening technological gaps between chip companies.

The nanometer figures that Hu discussed are called nodes, and they are,

for want of a better term, the mile markers of Moore’s Law. Each node

marks a new generation of chip-manufacturing technology. And the

progression of node names over the years reflects the steady progress

that both logic and memory chips have made: The smaller the number, the

smaller the transistors and the more closely they are packed together,

producing chips that are denser and thus less costly on a per-transistor

basis.

But the relationship between node names and chip dimensions is far from

straightforward. Nowadays, a particular node name does not reflect the

size of any particular chip feature, as it once did. And in the past

year, the use of node names has become even more confusing, as chip

foundries prepare to roll out 14-nm and 16-nm chips, custom-made for

smartphone makers and other customers, that will be no denser than the

previous 20-nm generation. That might be just a temporary hiccup, a

one-time-only pause in chip-density improvement. But it’s emblematic of

the perplexing state of the field.

Moore’s Law, when reflected through the steady march of node names,

might seem easy and inexorable. But today a plague of intense

manufacturing and design problems is forcing compromises that are

sometimes sobering. And some analysts suggest that regardless of what we

call the next generation of chips, the transition from old to new no

longer provides nearly the kind of payoff—in cost or performance—that it

used to. “What do you mean by 14 nm?” When I asked An Steegen that

question at an industry conference in July, she smiled and let out a

wry, knowing laugh. “Ah…what’s in a name?” asked Steegen, senior vice

president for process technology development at Imec, the Belgian research center. “Actually, not that much any more.”

It’s a state of affairs that has been nearly two decades in the making.

Once upon a time, the node name told you practically everything you

needed to know about a chip’s underlying technology. If you trained your

microscope on microprocessors made by a handful of different companies

using a 0.35-micrometer process, you’d find that their products were all

remarkably similar.

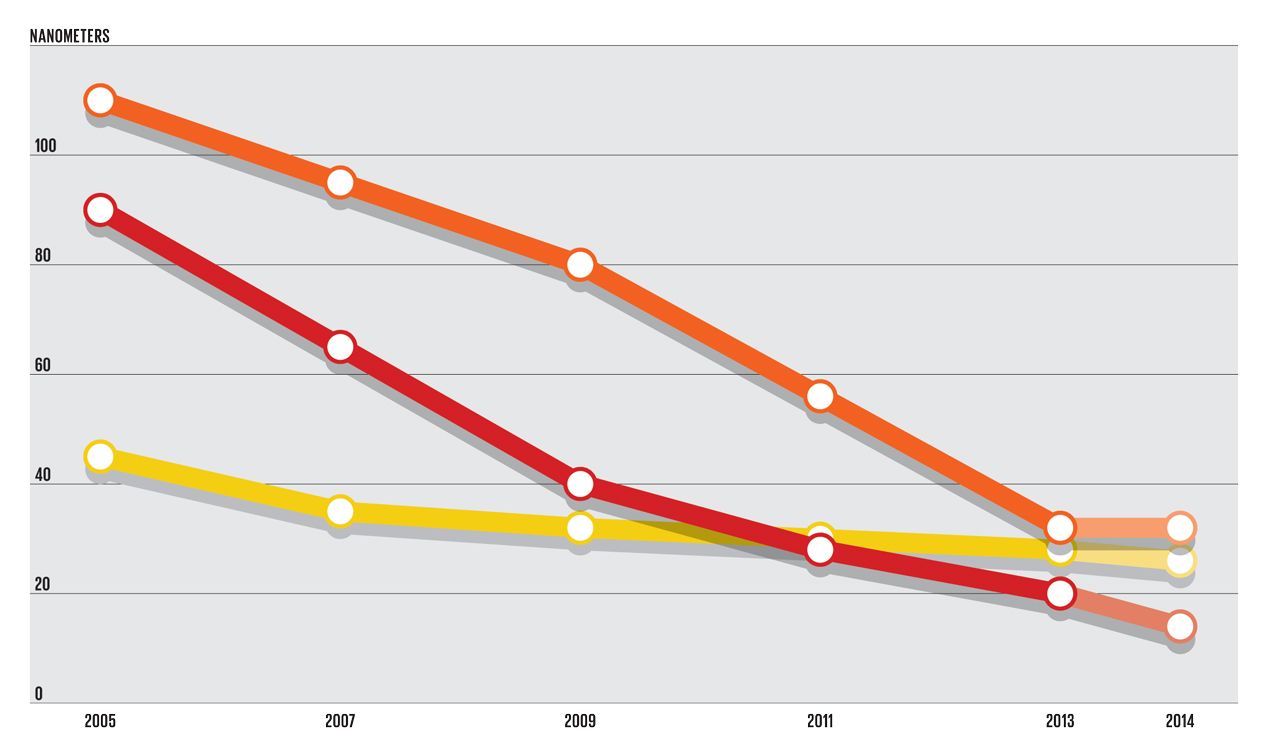

Data Source: GlobalFoundriesWhat’s in a name?

Key chip dimensions, such as the transistor gate length [yellow] and

the metal one half pitch [orange]—half the distance spanned by the width

of a wire and the space to the next one on the dense, first metal layer

of a chip—have decreased but not strictly tracked the node name [red].

These numbers, provided by GlobalFoundries, reflect the company’s plans

to accelerate the introduction of 14 nm chips in 2014, a good year

early.

In the mid-1990s, when such chips were the state of the art, 0.35 µm

was an accurate measure of the finest features that could be drawn on

the chip. This determined dimensions such as the length of the

transistor gate, the electrode responsible for switching the device on

and off. Because gate length is directly linked to switching speed,

you’d have a pretty good sense of the performance boost you’d get by

switching from an older-generation chip to a 0.35-µm processor. The term

“0.35-µm node” actually meant something.

But around that same time, the link between performance and node name

began to break down. In pursuit of ever-higher clock speeds, chipmakers

expanded their tool kit. They continued to use lithography to pattern

circuit components and wires on the chip, as they always had. But they

also began etching away the ends of the transistor gate to make the

devices shorter, and thus faster.

After a while, “there was no one design rule that people could point to

and say, ‘That defines the node name,’” says Mark Bohr, a senior fellow

at Intel. The company’s 0.13-µm chips, which debuted in 2001, had

transistor gates that were actually just 70 nm long. Nevertheless, Intel

called them 0.13-µm chips because they were the next in line. For want

of a better system, the industry more or less stuck to the historical

node-naming convention. Although the trend in the measurements of

transistors was changing, manufacturers continued to pack the devices

closer and closer together, assigning each successive chip generation a

number about 70 percent that of the previous one. (A 30 percent

reduction in both the x and y dimensions corresponds to a 50 percent

reduction in the area occupied by a transistor, and therefore the

potential to double transistor density on the chip.)

The naming trend continued as transistors got even more complex. After

years of aggressive gate trimming, simple transistor scaling reached a

limit in the early 2000s: Making a transistor smaller no longer meant it would be faster or less power hungry. So Intel, followed by others, introduced new technologies to help boost transistor performance. They started with strain engineering,

adding impurities to silicon to alter the crystal, which had the effect

of boosting speed without changing the physical dimensions of the

transistor. They added new insulating and gate materials. And two years ago, they rejiggered the transistor structure to create the more efficient FinFET, with a current-carrying channel that juts out of the plane of the chip.

Through all this, node name numbers continued to drift ever downward,

and the density of transistors continued to double from generation to

generation. But the names no longer match the size of any specific chip

dimension. “The minimum dimensions are getting smaller,” Bohr says. “But

I’m the first to admit that I can’t point to the one dimension that’s

32 nm or 22 nm or 14 nm. Some dimensions are smaller than the stated

node name, and others are larger.”

The switch to FinFETs has made the situation even more complex. Bohr

points out, for example, that Intel’s 22-nm chips, the current state of

the art, have FinFET transistors with gates that are 35 nm long but fins

that are just 8 nm wide.

That is, of course, the view from a chip manufacturer’s side. For his part, Paolo Gargini, the chairman of the International Technology Roadmap for Semiconductors,

says the node is and always has been defined by the proximity of wires

on the first metal layer on the back of the chip, a dimension that was

reflected well in DRAM and, later, flash memory, but not in logic.

Illustrations: Emily CooperTwo Transistors:

Chipmakers are in the process of moving from traditional planar

transistors [left] to ones that pop out of plane [right]. Intel

introduced these 3-D transistors in 2011, and they are now shipping

widely. The leading foundries, such as GlobalFoundries, Samsung, and

Taiwan Semiconductor Manufacturing Co., are in the process of ramping up

production of 20-nanometer planar transistors. They will make the

switch to 3-D with the next generation.

Regardless of definition, numbers in node names have continued

to decline. Along with them, the distance between transistor gates and

that between the closest copper wires on the back of the chip have also

decreased. Both of those features help define how dense a chip can be

and thus how many more you can produce on a single silicon wafer to

drive down costs.

But the difficulty inherent in printing ever-finer features has now

taken its toll. “When we got to around 28 nm, we were actually pushing

the limits of the lithographic tools,” says Subramani Kengeri,

vice president of advanced technology architecture at GlobalFoundries,

the world’s second-biggest chipmaking foundry after Taiwan Semiconductor

Manufacturing Co.

To deal with this, Kengeri and his colleagues were forced to adopt a lithographic technique called double patterning.

It lets technicians pattern smaller features by splitting a single

patterning step into two, relying on a slight offset between the two

steps.

Intel used the technique to form transistors on its 22-nm chips, but it

stuck to single patterning to make the densest metal layer. Pushing the

technique to its limits, the company made wires with a pitch of 80 nm,

which encompasses the width of one wire and the space to the next. By

adopting double patterning, GlobalFoundries and others could push the

pitch down to about 64 nm for their 20-nm chips. But that move came with

a significant trade-off: Double-patterned chips take longer to make,

adding significantly to the cost.

Carrying this technique over from the 20-nm node to 14 nm would mean

that chipmakers would have to double-pattern even more layers of the

chip. So last year, Kengeri and his colleagues announced a chip industry

first: They would put a stop to the shrink. GlobalFoundries’ line of

14-nm chips, which are slated to begin production in 2014, may be the

foundry world’s first FinFET transistors. But the company will build the

new chips with the same wiring density used in its 20-nm chips. “The

first-generation FinFET is basically reusing all of that and plugging a

FinFET into that framework,” Kengeri says. “It’s really a 20-nm FinFET,

in a way.” Nevertheless, the company refers to these as 14-nm chips

because they offer roughly a generation’s-worth jump in performance and

energy efficiency over its 20-nm chips.

Kengeri hopes that by putting a one-generation pause on shrinking chips

and focusing on introducing 3-D transistors, GlobalFoundries will catch up with Intel,

which is already shipping 3-D devices in its 22-nm chips.

GlobalFoundries’ 14-nm chips aren’t any denser than—and therefore cost

just about as much as—the previous generation, but they’re still a big

improvement, Kengeri says. “Our point—and our customers agree—is that as

long as they see that value, they don’t care what the technology is

called or what is inside.”

“It is quite a controversial move,” says William Arnold, chief scientist at ASML,

the world’s largest maker of semiconductor-fabrication equipment. “The

customers of the foundries, the people who are making cellphone parts,

are very skeptical of not being able to get a shrink along with a

performance improvement. They’re pretty vocal about saying that they’re

not happy about that.” The foundries’ latest move aside, chips are still more or less doubling in density from node to node, says Andrew Kahng,

a professor at the University of California, San Diego, and an expert

on high-performance chip design. But for Kahng, the steady progression

of node names masks deeper problems. There is a difference, he says,

between “available density” (how closely you can pack circuits and wires

on a chip) and “realizable density” (what you can actually put into a

competitive commercial product).

The sheer density and power levels on a state-of-the-art chip have

forced designers to compensate by adding error-correction circuitry,

redundancy, read- and write-boosting circuitry for failing static RAM

cells, circuits to track and adapt to performance variations, and

complicated memory hierarchies to handle multicore architectures. The

problem, Kahng says, is that “all of those extra circuits add area.” His

group has been scouring company specs and deconstructing images of

chips for years, and they’ve come to an unsettling conclusion: When you

factor those circuits in, chips are no longer twice as dense from

generation to generation. In fact, Kahng’s analysis suggests, the

density improvement over the past three generations, from 2007 on, has

been closer to 1.6 than 2. This smaller density benefit means costlier

chips, and it also has an impact on performance because signals must be

driven over longer distances. The shortfall is consistent enough, Kahng

says, that it could be considered its own law.

This might be a recoverable loss. So far, Kahng says, the chip industry

has made it a priority to keep up the pace of Moore’s Law, ensuring

that manufacturers can continue to build and release new product

families while using a new process every 18 to 24 months. This means

there hasn’t been time to explore a number of design tricks that could

be used to cut down on power or boost performance. “When you’re on that

kind of schedule, you don’t have time to optimize things,” he says. As

the value of the simple shrink decreases, he says, chipmakers should

then be able to revisit their designs and find chip-improving approaches

they may have missed or else left on the cutting-room floor.

When will the scaling stop? Today’s patterning technology, which relies

on 193-nm laser light, is becoming an ever more costly challenge, and

its natural successor, shorter-wavelength extreme ultraviolet

lithography, has been long delayed.

Kahng says chipmakers may face a more immediate struggle with wiring in

just a few years as they attempt to push chip density down past the

10-nm generation. Each copper wire requires a sheath containing barrier

material to prevent the metal from leaching into surrounding material,

as well as insulation to prevent it from interacting with neighboring

wires. To perform effectively, this sheath must be fairly thick. This

thickness limits how closely wires can be pushed together and forces the

copper wires to shrink instead, dramatically driving up the resistance

and delays and drastically lowering performance. Although researchers

are exploring alternative materials, it’s unclear, Kahng says, whether

they will be ready in time to keep up with Moore’s Law’s steady pace.

Many people in the industry, who have watched showstopper after

showstopper crop up only to be bypassed by a new development, are

reluctant to put a hard date on Moore’s Law’s demise. “Every generation,

there are people who will say we’re coming to the end of the shrink,”

says ASML’s Arnold, and in “every generation various improvements do

come about. I haven’t seen the end of the road map.”

But for those keeping track of the road, those mile markers are starting to get pretty blurry. A version of this article originally appeared in print as “The End of the Shrink.”

Aucun commentaire:

Enregistrer un commentaire